USDA still provides 100% mortgage financing in many parts of Texas. Homebuyers are surprised to learn exactly what locations are still considered “rural” eligible. The truth is some locations just outside the major cities like Houston, Dallas, Austin and San Antonio may still qualify for USDA financing today.

USDA loans are a perfect solution for TX first time home buyers that want to purchase their first home, but have limited funds to do so. Below we will look at the latest USDA mortgage requirements and the benefits it provides home buyers.

- NO Down Payment 100% Financing: Unlike most other types of mortgage financing, USDA mortgages in Texas require no down-payment which makes it easier for first-time home buyers to own homes.

- Less Than Perfect Credit Scores Possible: Because USDA 502 guaranteed loans are backed by the government, those with a “less than perfect” credit borrowers have an easier time getting approved for a USDA loan. As of 2024, the program requires a min 620 score to be approved by most lenders.

- Low 30 Year Fixed Interest Rates: Since USDA guarantees the loans against default, therefore USDA loans usually have better interest rates than most conventional mortgage loans. Also, since they are guaranteed by the federal government, lenders are more likely to offer the program. The USDA program is a standard 30-year fixed mortgage with no early payoff penalty.

- Low Monthly Mortgage Insurance (PMI): Monthly PMI is much less when compared to other FHA and conventional loan programs. In fact, the monthly mortgage insurance is almost half as less as the FHA loan.

USDA rural housing does have a few eligibility requirements, and understanding these requirements is very important. USDA household income and property location are the two keys. It is a good idea to find out the eligibility based on your household income and the location of the home you are planning on buying or refinancing.

At Coast 2 Coast we are happy to guide you through the entire process, we encourage any home buyers that have questions to call us or just submit the Quick Request Form on this page.

The USDA home loan has many different names. It is often called the USDA Rural Home Loan, Rural Development or 502 Guaranteed Home Loan. All USDA 502 loans are offered through approved USDA lenders only. Of course, 100% financing is the main benefit to USDA financing and even today it remains the only $0 down mortgage program (excluding the VA loan that is also available to Veterans) We will go over the most important USDA lending requirements below.

USDA Mortgage Eligibility

To be approved and eligible, borrowers must:

- Have an adequate and dependable income. A solid two-year job history is often needed.

- Be a U.S. citizen, qualified alien, or be legally admitted to the United States for permanent residence.

- Have an adjusted annual household income that does not exceed the moderate income limit established for the area. A family’s income includes the total gross income of the applicant, co-applicant and any other adults in the household. This includes members of the home earning income even if they are not included on the loan application for qualifying purposes. Applicants may be eligible to make certain adjustments to gross income— such as annual child care expenses and $480 for each minor child—in order to qualify. Please click here for the USDA income calculator.

- Have a credit history that indicates a reasonable willingness to meet obligations as due. 620 min credit score

- Have repayment ability based on the following debt to income ratios: Housing debt cannot exceed 30%. Total monthly obligations with housing / gross monthly income cannot exceed 42%.

USDA Property Eligibility:

You’d be surprised as to what homes are in USDA eligible areas. Reach out to us if you would like to discuss the USDA approved area around your town. Typically, towns on the outskirts of larger cities and less than 30,000 residents apply. Please click this link Property Eligibility and begin your search. If you have any questions, please contact us below.

- Guaranteed loans can be made on either new or existing homes; Existing homes must be structurally sound, functionally adequate, and in good repair. There are no restrictions on the size or design of the home financed.

- The home must be owner occupied and primary residence. Investor homes are not permitted. Property cannot be income producing (Farm, Cattle Ranch, etc)

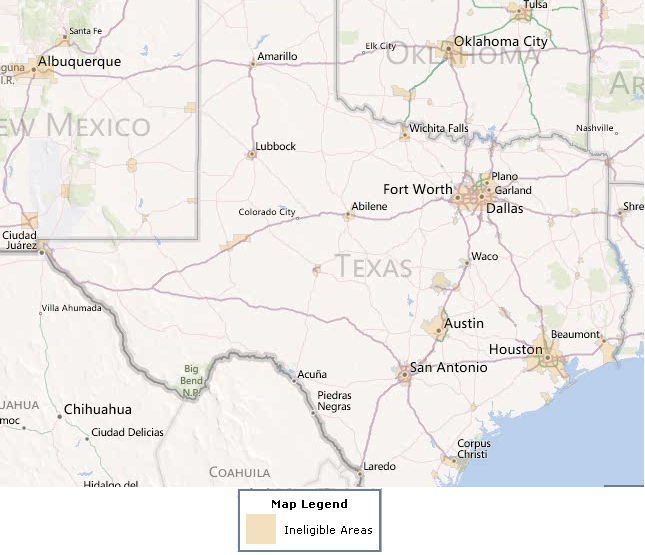

- Homes must be located in rural areas, check the map above. The seller of the home is not important, only where the property is located.

The map below shows the darker brown areas that are NOT USDA approved.

Highlights of the 100% USDA Loan Program:

- Loans may be for up to 100 percent (101% LTV if the 1.0 % guarantee fee is included in the loan) of appraised value or for the acquisition cost, whichever is less.

- $0 money down.

- Mortgages are 30-year fixed rate at market interest rates.

- Loans may include funds for closing costs, the guarantee fee, legal fees, title services, cost of establishing an escrow account and other prepaid items if the appraised value is higher than sales price. Sellers may contribute to the buyer’s closing costs.

- Home buyers make application with approved Texas USDA lenders. Please contact us if you would like to begin the process.

- Buyers must personally occupy the dwelling following the purchase.

- Loans may be made to refinance either existing USDA Rural Development Guaranteed housing loans or our Section 502 Direct housing loans.

Want to learn more? Please reach out to us 7 days a week. For quick service just submit the Quick Request Form found on this page.